Travel booms when households have jobs, rising income and time to use both. That has basically been the story of the rise of leisure travel over the past 250 years.

The Industrial Revolution increased output: Henry Ford’s five-day workweek helped turn higher productivity into more leisure time, while rising wages and paid time off did the rest. Over generations, productivity gains became hotel stays, flights, restaurant meals, attraction visits, cruises and vacation rental trips.

Artificial intelligence (AI) is the next productivity shock, and for travel, the question is not just how much output it creates but where the gains go. Said another way, if AI increases productivity, it will make the economy bigger; the question is whether that growth turns into jobs, disposable income and time.

As an economist, when I forecast travel demand, I usually come back to two variables: jobs and income. If people have jobs and their disposable income is growing, they travel. If either side of that equation weakens, travel feels it quickly.

That is why the AI debate matters so much: If AI raises productivity and those gains show up in employment, disposable income and flexibility, travel could be one of the biggest beneficiaries. If AI increases output while the number of employed people declines, the industry faces a very different demand environment.

Most travel AI conversations today focus on the parts companies can control: pricing, revenue management, guest messaging, marketing, customer service, partner reporting and back-office automation. Those tools matter, and the companies that use them well will have a real cost advantage.

But that is only half the story. The harder question is what AI does to the traveler: Do they have a job? Is their disposable income growing? Do they have time off? And how do they search and book?

Vacation rentals are a useful example because they are as close to pure-play leisure demand as travel gets. When jobs and disposable income move, short-term rental demand tends to show it clearly.

The real AI debate is about distribution

The downside case is not complicated: Companies spend heavily on AI infrastructure and software, margins get pressured, workers get displaced and income growth weakens. Household spending slows, revenue disappoints and more layoffs follow.

Citrini Research framed that risk earlier this year in a widely discussed 2028 scenario: 10.2% unemployment, a 38% peak-to-trough drop in the S&P 500 and labor’s share of national income falling from 56% to 46% in four years. I would not treat that as a forecast, but I would not ignore it either. History has examples where productivity rose before workers benefited. In Britain from the 1770s to the 1830s, productivity increased for decades while real wages stagnated, a period economists call the Engels’ Pause.

The gains eventually diffused, but only after political and institutional pressure changed the distribution.

The optimistic case is just as credible. Citadel Securities, Alex Imas at the University of Chicago and a16z all argue, in different ways, that AI should act as a positive supply shock. It lowers costs, raises real incomes, creates new work and shifts spending toward services, experiences and other things that remain scarce when software gets cheap.

That argument matters a lot for travel. If productivity turns into jobs and rising disposable income, travel gets the upside. As households get richer, they tend to spend more on experiences and services where the human element still matters: hospitality, dining, entertainment, wellness and personalized trips. In that world, AI does not shrink travel. It expands the market.

My view is optimistic: AI-driven productivity growth is more likely to be a long-term tailwind for travel than a threat, but the downside case is plausible enough that it should be planned for, not hand-waved away. There is also a policy backstop worth considering. If displacement accelerates, governments and companies will come under pressure to maintain consumption. OpenAI has floated 32-hour, four-day workweek pilots with no pay cut as one possible response.

For travel, that matters: AirDNA data show Fridays already sell roughly 20% more short-term rental nights than Thursdays in the U.S., which gives some sense of what another non-work day could mean for leisure demand.

What the scenarios mean for travel demand

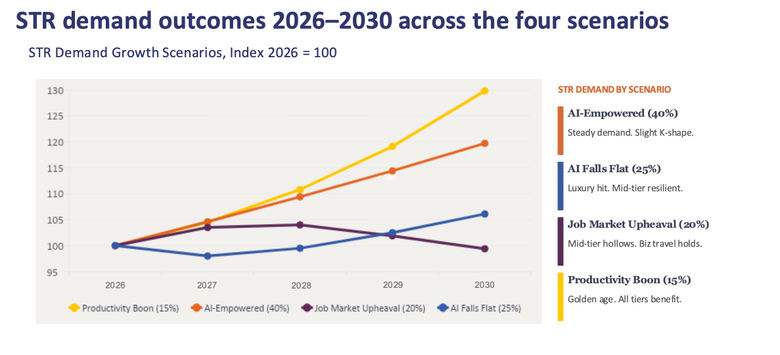

Moody’s Analytics published a useful framework in February with four possible AI paths: an AI Empowered Economy, a Productivity Boon, AI Falls Flat and Job Market Upheaval.

The first two are upside cases: productivity rises, employment holds, real incomes improve and consumers spend more on leisure.

The third is a dot-com-style disappointment, where heavy AI infrastructure spending fails to deliver a meaningful productivity payoff.

The fourth is the displacement case, in which productivity rises, but jobs, labor income and household spending weaken.

AirDNA translated those macro paths into a travel-specific view using our U.S. short-term rental forecasting model, and the spread was wide. The two upside scenarios produced 20% to 25% demand growth over five years. The two downside scenarios produced flat demand at worst through 2030. Combined, those downside scenarios carried a 45% probability in Moody’s framework.

Source: AirDNA, Moody's Analytics scenarios

Vacation rentals are useful here because they are a high-beta read on leisure travel. Roughly 85% of short-term rental nights are leisure-driven, with less insulation from corporate, group or non-discretionary demand than hotels, airlines, restaurants, tours or attractions. If AI produces a K-shaped economy, the damage will not land evenly. A 10% employment shock would not necessarily imply a 10% decline in travel demand. Depending on which workers lose jobs and income, the impact on mid- and lower-tier leisure travel could be greater.

That spread should change how the travel industry talks about AI. A company can use AI to cut costs, optimize pricing, improve conversion and still struggle if the middle of the traveler economy weakens. If productivity gains diffuse broadly, the same company could be operating in one of the strongest leisure demand environments we have ever seen. Both paths are possible, and planning for only one is the real risk.

AI agents will change who gets the booking

AI will also change travel demand in a second way: not just who can travel, but who gets chosen when they do.

When AI agents do the searching, the old discovery funnel begins to break down. Travelers may no longer scroll through pages of listings, adjust filters, compare tabs, read dozens of reviews and return to the same familiar online travel agency (OTA). They may simply tell an agent what they want: a nonstop flight, a family-friendly hotel, a pet-friendly home near the beach, a guided tour or the best total trip cost for a family of five.

AI agents do not have a home screen; they do not feel loyalty the way humans do. They can compare loyalty programs, fees, policies, availability, amenities, reviews and rates across platforms in seconds. Platform fees and OTA take rates that once felt fixed become part of the optimization problem.

For travel suppliers and intermediaries, clean data becomes a competitive advantage. Accurate amenities, structured descriptions, real-time availability, transparent fees, flexible application program interfaces (APIs), loyalty logic, policies and direct-booking connectivity matter more when a machine is interpreting the product on behalf of a human.

This is the next version of search engine optimization (SEO). In the Google era, companies optimized for search engines. In the AI-agent era, companies will need to make their inventory easy for machines to understand, compare, price, trust and book.

What travel leaders should do now

Lower the cost base, but automate friction, not hospitality. Travel companies should move quickly to implement AI across operations, marketing, revenue management, customer service, guest communication, finance and reporting. But the test should not be simply, “Can this be automated?” The better question is whether automation removes friction or removes something travelers actually value. A check-in code can be automated. A thoughtful host, a great guide, a front-desk team that solves a real problem or a local recommendation that changes the trip may still be the product.

Underwrite demand through jobs and income, not just travel trends. The key AI risk is not only slower bookings. It is productivity gains that fail to show up in employment and disposable income. Travel leaders should track payroll growth, unemployment claims, disposable income growth, household confidence, lead times, booking pace, average daily rate (ADR) resistance and cancellations. Waiting for consensus is usually waiting too long.

Prepare for AI agents to become a booking channel. If AI agents begin shaping travel search, clean inventory data becomes a distribution infrastructure. Amenities, policies, fees, availability, rates, loyalty rules, APIs and direct-booking connectivity need to be structured, accurate and machine-readable.

My bet

My bet is that AI-driven productivity growth becomes one of the biggest long-term tailwinds the travel industry has ever seen. More productivity should mean more jobs in new categories, more disposable income, more flexibility and more spending on experiences. Vacation rentals, with their exposure to leisure travelers, families, groups, longer stays and local experiences, show how powerful that upside could be.

Even the downside case may eventually create policy responses that support travel demand, but operators cannot build a strategy around waiting for those responses. Optimism is not the same as complacency. AI could give travel a stronger customer, one who is employed, more flexible and with more disposable income to spend on experiences, but the risk is that it first gives us a more fragile one. The companies that win will be the ones that use AI aggressively inside the business while watching just as closely for weakness in the traveler outside it.

About the author ...

Jamie Lane is the chief economist for

AirDNA.